Too-big-to-fail regulations: Federal Council adopts dispatch and Capital Adequacy Ordinance

Bern, 22.04.2026 — During its meeting on 22 April 2026, the Federal Council adopted the dispatch on the revision of the Banking Act. In the future, systemically important banks in Switzerland will have to fully back their participations in foreign subsidiaries with Common Equity Tier 1 (CET1) capital. This targeted measure is key to strengthening financial stability. Parliament will be able to debate the legislative proposal from summer 2026. At the same time, the Federal Council amended the Capital Adequacy Ordinance. The amendments concern the capital backing for certain balance sheet items such as software, and will come into force on 1 January 2027. The solution proposed by the Federal Council is more moderate than planned, due to the results of the consultation procedure. In terms of capital requirements, the result is thus a balanced overall package that takes account of the comments received.

At present, the foreign participations of systemically important banks are not adequately backed by CET1 capital. This became apparent in the Credit Suisse case in 2023, and contributed significantly to the fact that the bank was unable to recover without assistance. Ultimately, in addition to the takeover by UBS, state intervention was needed to avert a financial crisis. This gap in the too-big-to-fail regime is now to be remedied with full backing with CET1 capital for foreign participations.

Systemically important banks should be able to dispose of foreign subsidiaries either in part or in whole during the recovery phase of a crisis, when they can still act autonomously, without negative impacts on the capital ratios of the parent bank. This is intended to reduce the likelihood of such banks needing to be wound down. This will strengthen the stability of global systemically important banks (G-SIBs) and thus also that of the Swiss financial centre. In addition, potential damage for taxpayers will be reduced.

The corresponding proposal to amend the Banking Act takes account of the recommendations of the Parliamentary Investigation Committee (PInC).

In the consultation, the objective of the proposal to further strengthen financial stability was generally welcomed. Around a third of participants supported the Federal Council's proposal, while others were in favour in principle, but called for adjustments. Most parties fall into these two categories. The other participants in the consultation procedure, including various banking and business associations, some cantons and the Swiss People's Party (SVP) and the Swiss Green Liberal Party (glp), rejected it.

The proposal now submitted to Parliament stipulates that, in the future, systemically important banks will have to fully back the carrying value of their participations in foreign subsidiaries with the Swiss parent bank's CET1 capital. Today, by contrast, around half can be financed with debt. Any valuation losses on foreign subsidiaries currently reduce the capital ratios of the Swiss parent bank from the very first Swiss franc. The new solution will prevent this, thereby reducing the likelihood of resolution or the need for state intervention, and ensuring that the risk is borne by shareholders rather than taxpayers. The Federal Council intends to allow for a transition period of seven years if there are no delays during the parliamentary deliberations. The Swiss National Bank (SNB) and the Swiss Financial Market Supervisory Authority (FINMA) support the proposed solution as well.

The Federal Council also examined other options based on comments made by the Swiss Social Democratic Party (SP) and the SVP during the consultation. However, it considers alternative measures such as a general increase in capital requirements (e.g. by applying a leverage ratio of 15%) or structural adjustments such as the separation of the US business to be disproportionate. At the same time, it considers only partial backing with CET1 capital to be ineffective. Therefore, the Federal Council believes that the proposal submitted is a balanced compromise.

Amendments to the Capital Adequacy Ordinance

With regard to the Capital Adequacy Ordinance (CAO), most participants in the consultation procedure rejected the Federal Council's proposals regarding deferred tax assets and software. The parliamentary Economic Affairs and Taxation Committees also recommended that the Federal Council align these measures more closely with international standards. The Federal Council has therefore decided not to require full backing with CET1 capital for deferred tax assets and software. Instead, there will be a maximum three-year amortisation period for software, in line with the EU regulations. The new arrangement is also limited to systemically important banks. The proposed change in the area of deferred tax assets has been dispensed with for the time being. Although it too would strengthen financial stability, it would be an exception internationally. Moreover, the risk reduction sought with this measure is also largely achieved with the capital backing for foreign participations proposed in the Banking Act. Should the latter not be sufficiently implemented, the Federal Council reserves the right to reassess the capital backing for deferred tax assets.

Finally, the Federal Council has decided not to proceed with the proposed adjustments to AT1 capital instruments for the time being, as it considers it more appropriate to await the international developments that are currently under way in this area. With regard to the Liquidity Ordinance, the Federal Council is limiting the new requirements concerning the provision of information in the event of liquidity shortages to systemically important banks. The ordinances will come into force on 1 January 2027; a transition period of two years will apply for the regulatory treatment of software. A decision by Parliament is not required for this.

Impact

With one exception, the new provisions in the act and ordinance affect solely systemically important banks. Only with regard to balance sheet items that are difficult to value will a few larger non-systemically important banks also have to fulfil stricter requirements.

Currently, only UBS is affected to a significant extent. The capital increase resulting from the ordinance already covers part of the statutory capital requirements for foreign participations. Both the increase in capital requirements and the additional capital need depend on future developments and strategic decisions by the bank, such as various buffers and limits set by management, the size and structure of UBS, the business model, the future scope of foreign business, the valuation of participations in foreign subsidiaries or their capital needs. In the case of UBS, according to the authorities' estimates and based on the status quo, the new regulations would lead to a substantial, targeted strengthening of the parent bank's CET1 capital by approximately USD 20 billion. If the regulations had been introduced on 1 January 2026, the actual CET1 shortfall would have been only around USD 9 billion.

If the financing costs are passed on in line with the principle of causality, they should not be borne by clients in Switzerland. Cross-subsidising the business of foreign subsidiaries with income from the domestic lending business would contradict the assumption of an efficient, competitive Swiss credit market.

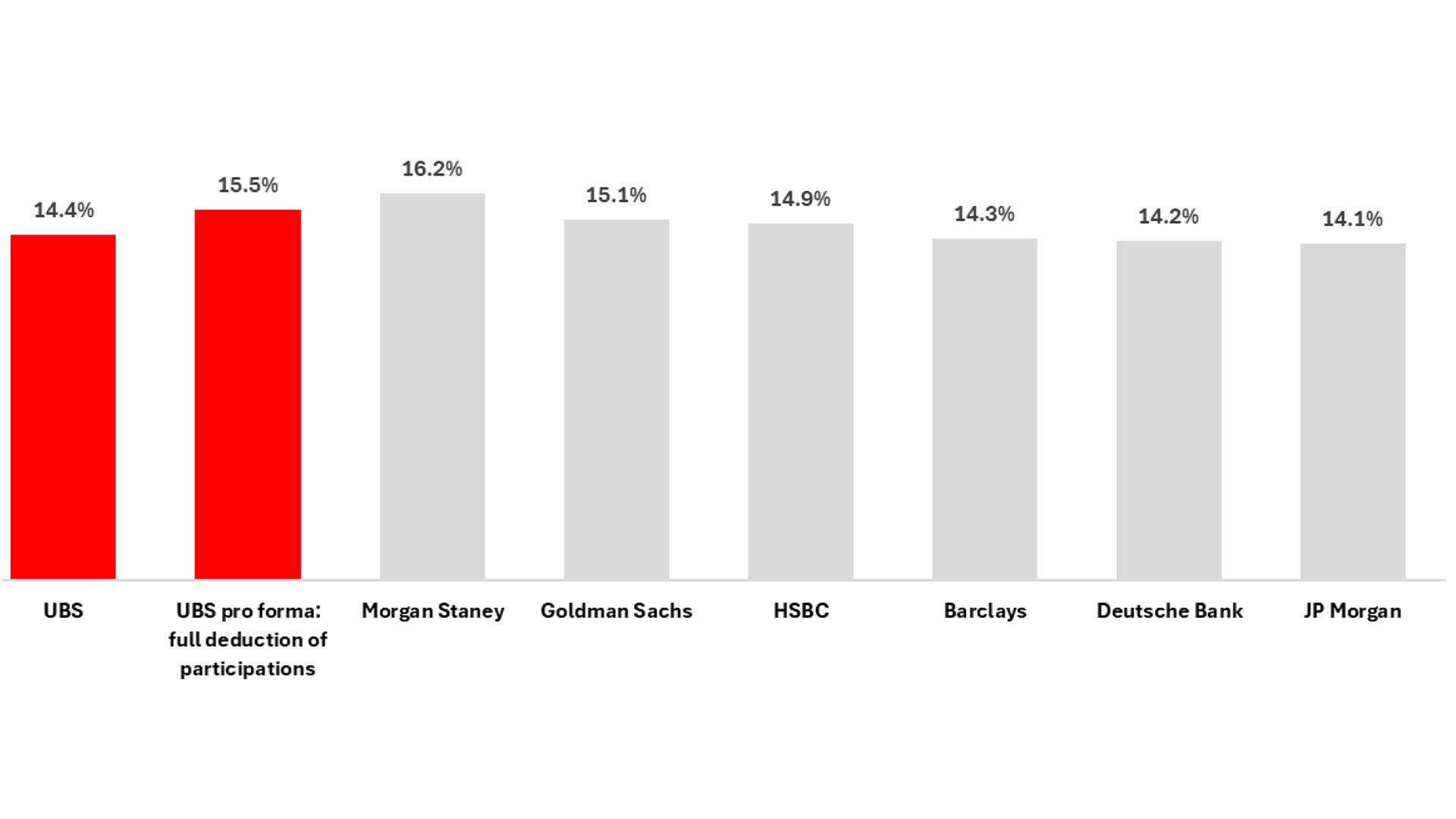

Following the implementation of all measures, the possible future CET1 capital ratio of UBS Group based on the pro forma calculation is 15.5%, which is in line with the current capital ratios of international peers. At Group level, this corresponds to a CET1 capital ratio increase of around 1.1 percentage points compared with the fourth quarter of 2025.

The Federal Council, the SNB and FINMA agree that the proposed package of measures is appropriate, necessary and targeted, as well as manageable for UBS.

International comparison of CET1 ratios

Appendix

Botschaft Änderung Bankengesetz

Bankengesetz

Ergebnisbericht Vernehmlassung zur Änderung des Bankengesetzes

Eigenmittelverordnung

Erläuternder Bericht zur Eigenmittelverordnung

Ergebnisbericht Vernehmlassung zur Änderung der Eigenmittelverordnung

Rechtliche Kurzanalyse Prof. Corinne Zellweger-Gutknecht zur Abspaltung des US-Geschäfts von systemrelevanten Banken